Moody’s , favorable con los bancos españoles

Maria Cabanyes, analista senior en Moody’s. - Miercoles, 21 de Enero

Moody’s ha publicado un informe sobre la banca española, que conoce una estabilización de los niveles de los préstamos en mora en sus balances. Moody’s cree que los préstamos en mora han alcanzado a un pico y, mientras que un cambio siginifcativo sea poco probable, el retorno al crecimiento economico y la caída del desempleo van a mejorar las perspectivas de los bancos españoles. Moody’s también está viendo una desaceleración en el ritmo de la disminución de los precios de la vivienda, mientras que la tendencia para el apalancamiento de los hogares está mejorando.

Leading Indicators Signal Peak in

Spanish Banks' Problem Loan Levels

Summary

The following report is a supplement to the special comment “Leading Indicators of Asset-Quality for Banks

in Western Europe” published on 16 December 2013.

The leading indicators we track to assess the health of the Spanish banking sector point

to a stabilization in the level of Non-Performing Loans (NPL) on banks' balance sheets

- the most pressing problem for the country's financial institutions since the onset of the

economic crisis. While a significant turnaround in the level of NPLs is unlikely in the

near future, we believe they have reached their peak. The return to economic growth

and falling unemployment is boosting business and consumer confidence, further

bolstering banks' prospects. We are also seeing a slowdown in the pace of house price

declines, while the trend for households' leverage is improving - even though the total

indicator readings are still weak.

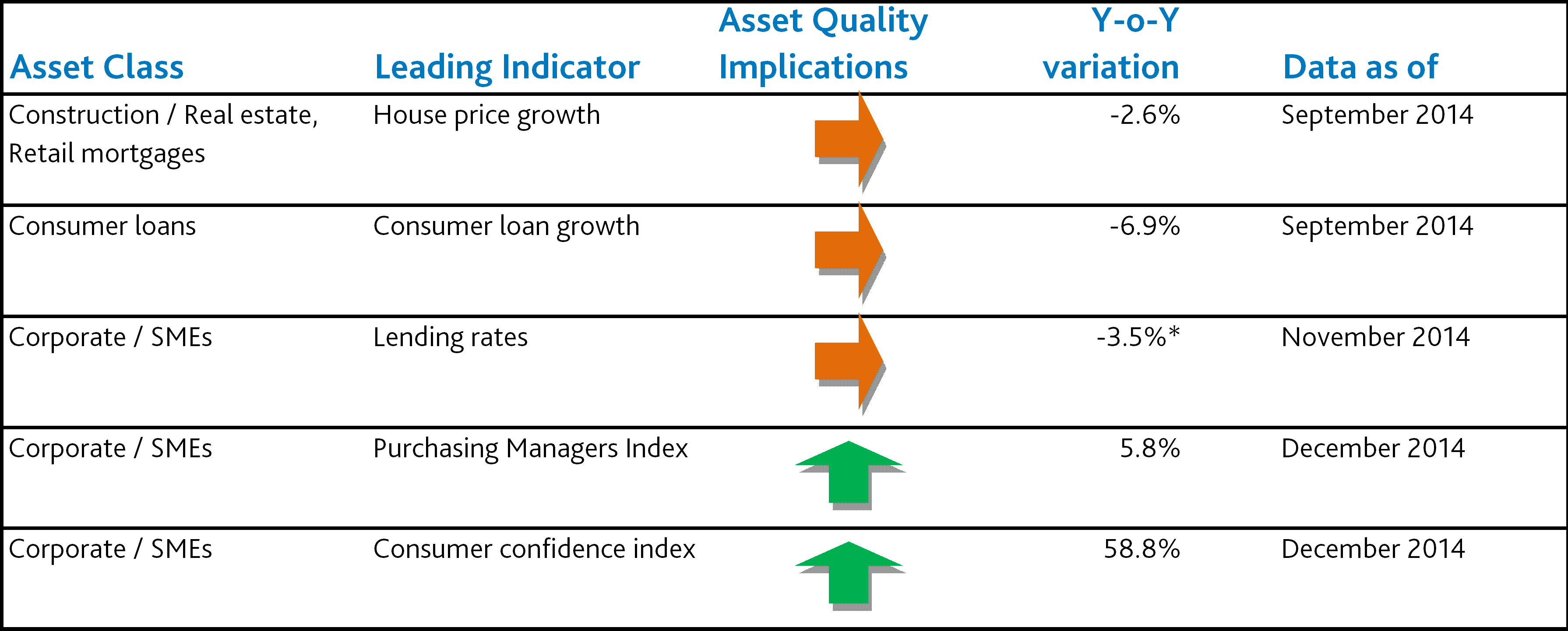

Note: In the column “Asset Quality Implications” we indicate our expectation of the future trend for problem loans in the next

12-18 months. Red downward arrows indicate asset quality deterioration, green upward arrows indicate improvement, and

orange arrows indicate stability/uncertainty. *Calculated as 2014 average lending rate relative to 2013 average lending

Recent Results and Long Term

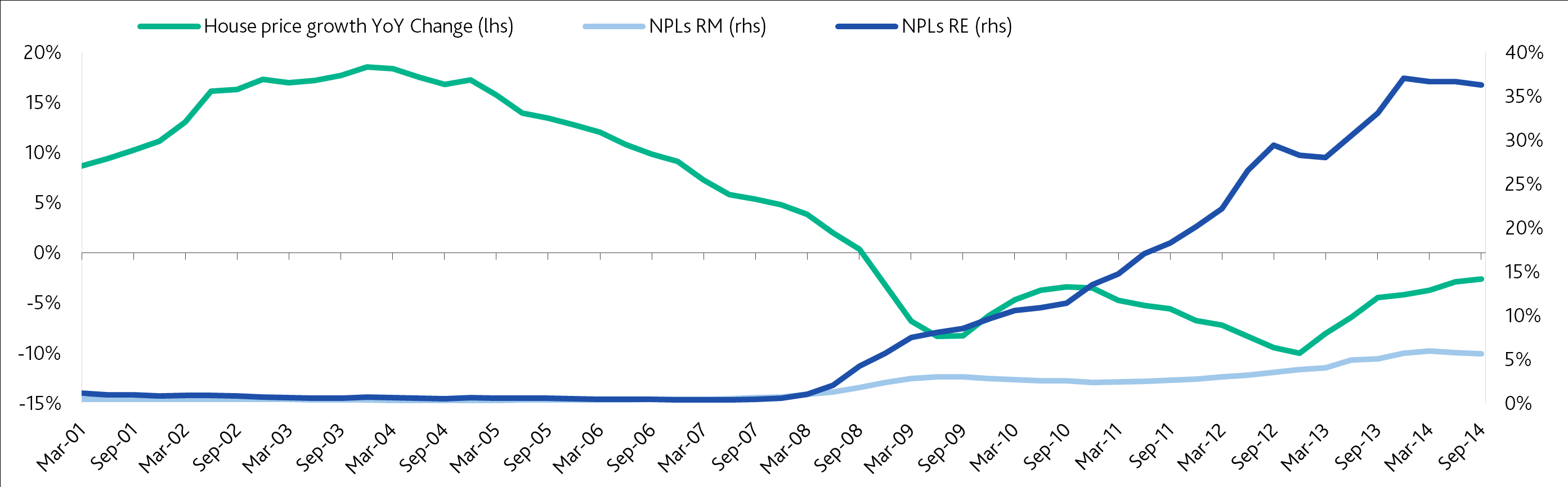

Our first leading indicator – residential real estate prices - is finally stabilizing after house prices slumped by almost a third in

the past seven years. While it merely shows that the pace of property price declines has been slowing over recent quarters rather

than a recovery in prices, it still gives us comfort. To us it signals that the stock of bad housing loans and problem loans made to

residential property developers will grow at a much weaker rate in the near future.

While the collapse of the construction boom in early 2008 has pushed down residential real estate prices by 30% up to now,

according to data from the Spanish ministry of Development, the speed of the decline has been much weaker in the past two

years. In December 2012 the annual decrease stood at 10.0%, a year later house prices fell by 4.2%.

We have seen a similar trend with the stock of consumer loans which had grown rapidly over several years preceding the crisis

until peaking in 2008. Between 2000-07, lending to consumers grew at annual rates of between 10%-20%, with the volume

of outstanding consumer loans almost tripling. Since its peak in 2008 the stock of consumer loans has fallen by 36%, bringing

households' leverage levels closer to the European Union average.

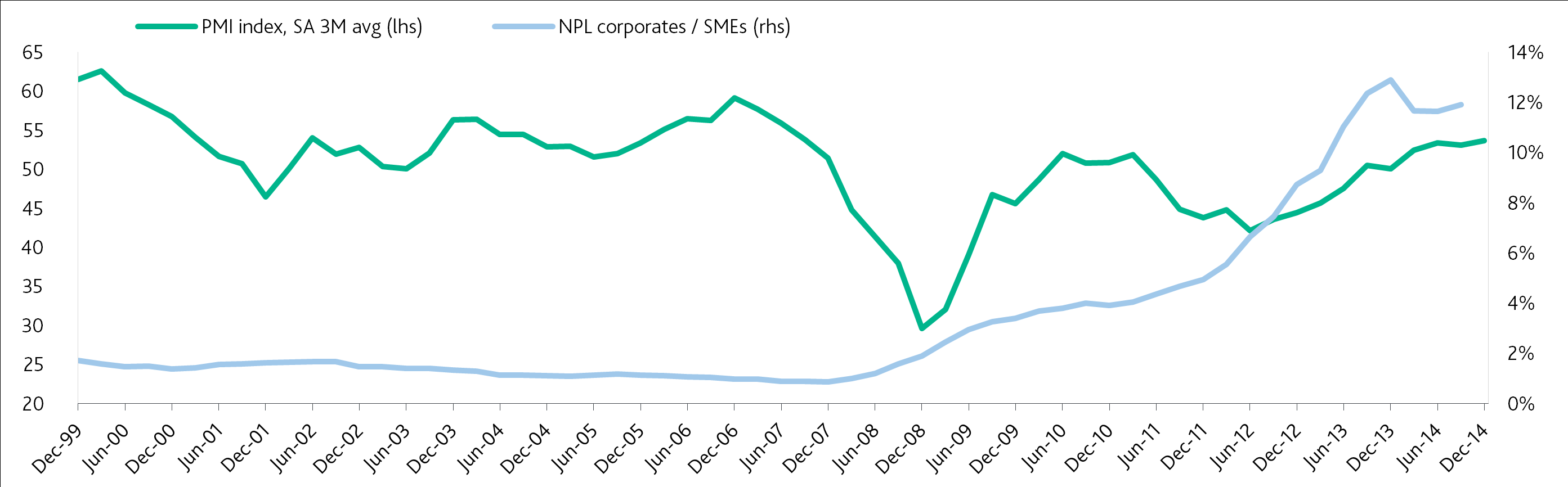

On a more positive note, the manufacturing Purchasing Manager's Index (PMI), a key forward-looking indicator measuring

the health of the manufacturing sector, has been rising since June 2013, reaching a reading of 54 in December 2014 (a reading

above 50 signals economic expansion) - a massive improvement from September 2008 when it plummeted to 30. We should

note, however, that the performance of this index shows a degree of volatility which complicates identifying clear trends.

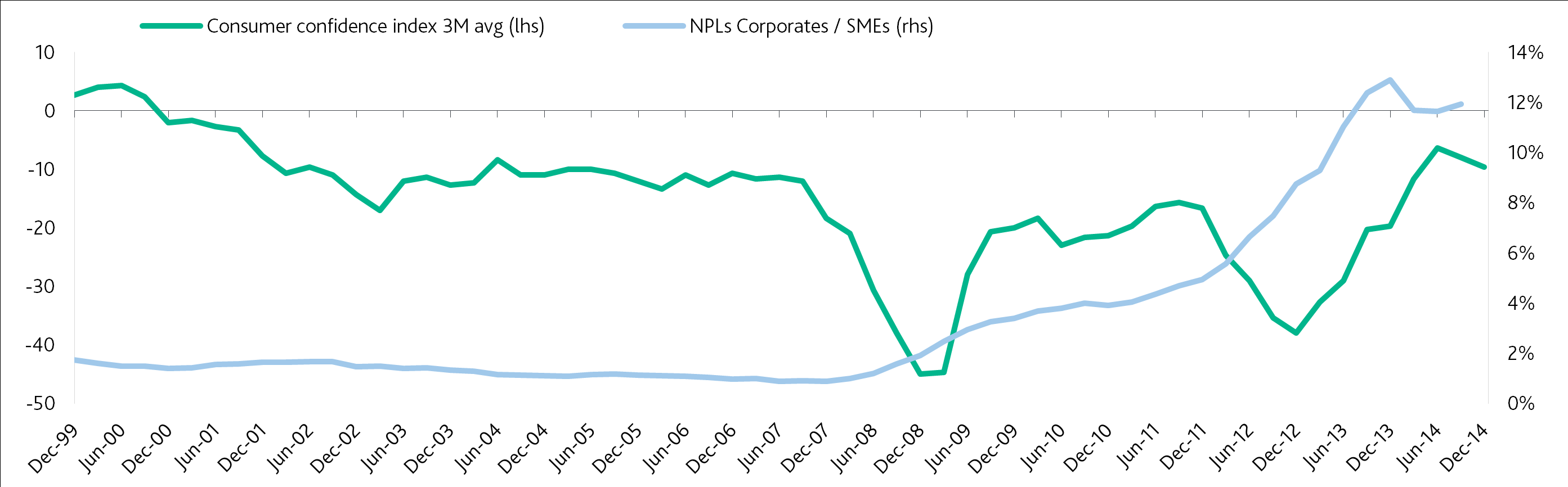

Another encouraging signal is provided by the Consumer Confidence Index, which tells a similar story to the PMI: a recovery in

the index since December 2012 after a big dip. The overall recovery of the Consumer confidence Index makes up close to 80%,

comparing the value registered in December 2008 (the lowest of the index since 1999) and the level reached in December 2014.

The index currently stands at pre-crisis levels, as consumers are more optimistic about their future economic situation.

Our final tracked indicator – lending rates for non-financial corporations - remains neutral. After peaking in September 2008,

borrowing costs have come down to levels similar to the pre-crisis period and have remained relatively stable for the past three

years.

These indicators, which we deem neutral or positive, together with our expectations for a moderate economic recovery lead us to

conclude that Spanish NPLs have already reached their peak and will from now on stabilize or even slowly decline. Having said

that, the stabilization process will take time and a significant reduction of the NPL stock is unlikely in the near future. This will

mostly hinge on the speed and resilience of the economic recovery.

What the Indices and NPLs Tell Us – Stabilization Story

The Neutrals

House Price Growth

This leading indicator reflects the overall state of the housing market, and allows us to identify house price bubbles that can

adversely affect the future performance of the residential mortgage and commercial real estate segments.

After several years of strong growth, the sharp decline in Spanish house prices, which started in 2008, reduced householders'

equity value in their homes, reducing their incentive for to service their debt. Likewise, strong house price growth pre-crisis

fuelled housing construction; this resulted in an oversupply and bankrupting many of the country's real estate developers.

This exposed banks to a massive growth in residential mortgage and commercial real estate loan arrears, with the arrears for

commercial real estate increasing much more dramatically.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

3 20 JANUARY 2015 SPANISH BANKS: LEADING INDICATORS SIGNAL PEAK IN SPANISH BANKS' PROBLEM LOAN LEVELS

The current trend in the indicator shows that, although house prices are still falling, over the last two years the pace of the

year-over-year price declines is slowing. The imbalance between housing supply and demand is reducing, as new housing

construction has been almost negligible since 2009 and statistics show a recovery in the number of housing transactions1 in the

last two years. This indicates that downward pressure on the performance of residential mortgages and commercial real estate

loans - the latter being one of the principal drivers of Spanish banks’ asset quality deterioration during the crisis - is easing.

In June 2014, nonperforming loan levels for residential mortgages fell for the first time in four years, dropping by 22 basis

points compared to the previous quarter2 . Altogether, all previously mentioned trends point to a future stabilization in

residential mortgage NPL ratios. Our view of a stabilization is also supported by the full recourse nature of residential mortgages

in Spain, which is a mitigating factor limiting the negative impact of the economic situation and high unemployment on asset

quality deterioration.

In terms of lending to real estate and construction companies, the arrears for this asset class decreased for the first time in six

years in March 2014 (not taking into account the decreases due to a transfer of real estate assets to Sareb3 in December 2012

and February 2013) and decreased slightly again in September 2014 to 36.3%. For this particular asset class we also expect a

stabilization, but with no significant reduction in NPL rates in the near future because of the oversupply of properties in the

market.

House price decline is slowing

Source: Ministry of Development, Bank of Spain

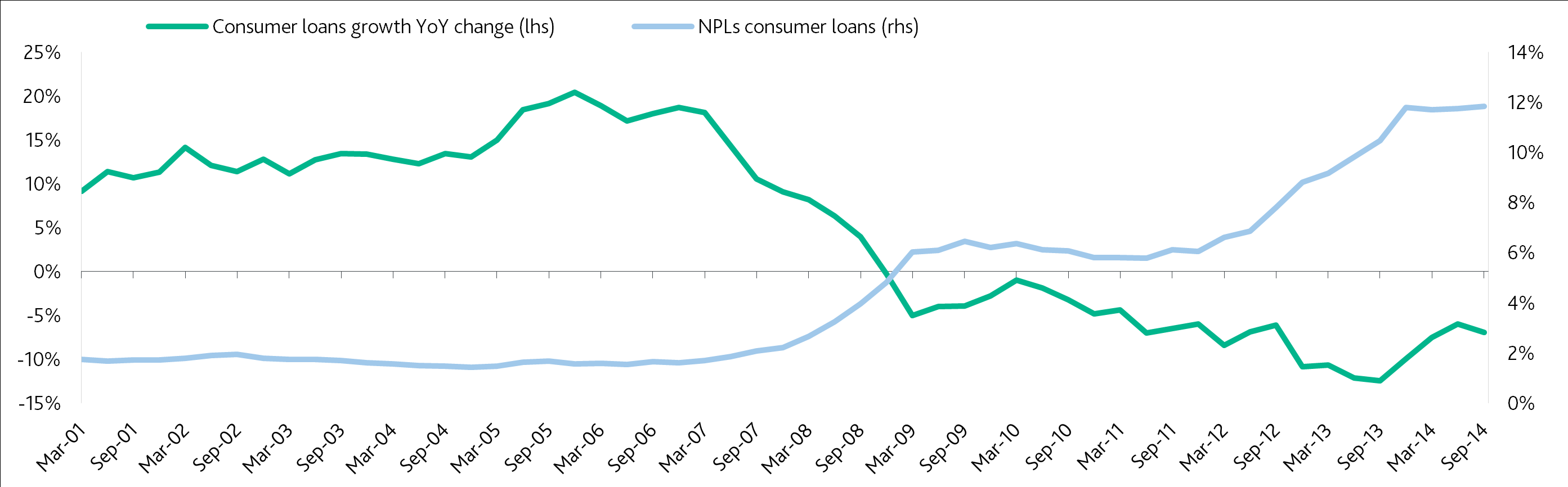

Consumer Loan Growth

This indicator is used to monitor NPLs coming from banks’ exposure to retail consumer loans. Strong growth in consumer

lending can serve as an early warning sign of loosening lending standards; in addition it poses a credit risk because of the

increase in households' leverage. It can also mask the impact of credit issues in the NPL ratio through the rapid growth of the

denominator.

A dramatic increase in consumer lending between 2000-07 - when lending to consumers grew at annual rates of between

10%-20% - was followed by a surge in arrears once the economy faltered. By the end of 2013, NPLs in this segment had

multiplied by four compared to the amount as of the end of 2007.

Consumer NPLs stabilised in March 2014, following a period of decline in the volume of consumer loans - especially acute in

2012 and 2013 - with positive implications for households' leverage and which also indicates a tightening in consumer lending

standards. The pressure on the performance of this segment should ease further.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

4 20 JANUARY 2015 SPANISH BANKS: LEADING INDICATORS SIGNAL PEAK IN SPANISH BANKS' PROBLEM LOAN LEVELS

Our expectation for consumer NPLs is supported by a brighter economic outlook and lower unemployment4 (Spain returned

to growth in Q3 2013 and unemployment started to decrease in Q2 20135 ), which should help to improve the performance of

household debt.

Consumer lending is returning to more normalised levels

Source: Bank of Spain

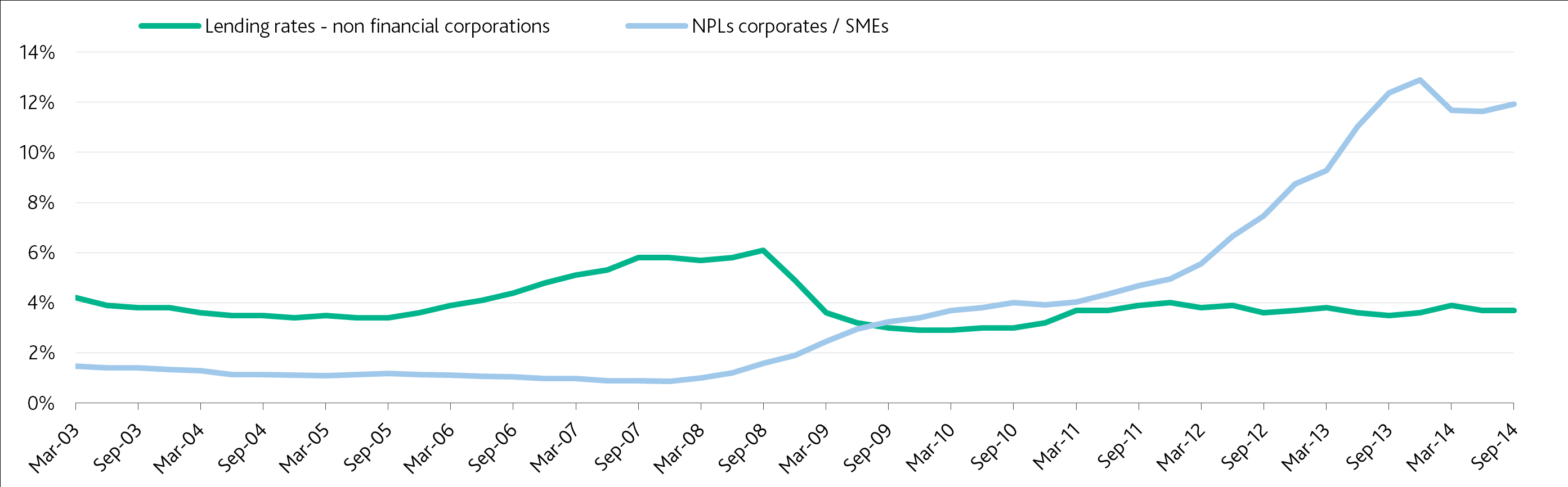

Non-financial Corporations Lending Rates

We track this indicator as higher lending rates imply more onerous debt-servicing costs thus translating into higher

delinquencies for the corporate sector. The indicator therefore correlates to the performance of corporate NPLs.

In recent years, low interest rates have helped offset the negative impact of Spain’s deep and lengthy recession on corporate loan

performance, easing the repayment burden for companies. The impact has been more favorable on secured loans, as they usually

have adjustable rates.

This indicator has remained stable over the last few years, and we expect it to maintain this trend in the foreseeable future

given the current low interest rate environment. In consequence, we do not expect that corporate NPLs will rise due to higher

borrowing costs.

We expect corporate lending rates to remain stable

Source: Bank of Spain

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

5 20 JANUARY 2015 SPANISH BANKS: LEADING INDICATORS SIGNAL PEAK IN SPANISH BANKS' PROBLEM LOAN LEVELS

The Positives

Purchasing Managers Index

This indicator reflects the health of the manufacturing sector and anticipates changes in the credit performance for corporates

and small and medium sized enterprises (SME). For most of the crisis the index has kept a reading of below 50, signaling

contraction. It started to recover in December 2012 and exceeded the 50 mark in the second half of 2013, pointing to a return

of growth in the sector.

The recovery in the manufacturing sector translates into greater business activity and improving companies' finances. This eases

pressure on the corporate NPLs ratio, which has retreated from its peak of 12.9% in December 2013to 11.9% in September

2014. As the economic recovery continues and the operating environment for Spanish companies improves we expect a further

slow decline in corporate NPLs.

PMI Index has recovered and keeps above 50 throughout 2014

Source: Haver, Bank of Spain

Consumer Confidence Index

This indicator tracks consumer expectations about their future financial situation, general economic development,

unemployment expectations and savings. This indicator started to recover in March 2013, and has recently returned to pre-crisis

levels. The significant recovery indicates overall optimism and a recovery of private consumption dynamics.

This index is similar to the PMI in that it is more volatile than the other indicators we track; however both signal an improving

trend in the operating environment in Spain and support our forecast of a slow reduction in corporate delinquencies rates.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

6 20 JANUARY 2015 SPANISH BANKS: LEADING INDICATORS SIGNAL PEAK IN SPANISH BANKS' PROBLEM LOAN LEVELS

Consumer confidence is recovering and approaches pre-crisis levels

Source: Bank of Spain

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

7 20 JANUARY 2015 SPANISH BANKS: LEADING INDICATORS SIGNAL PEAK IN SPANISH BANKS' PROBLEM LOAN LEVELS

Endnotes

1 NPLs per asset class are only reported quarterly.

2 Sociedad de Gestión de Activos Procedentes de la Reestructuración Bancaria, a government-initiated “bad bank”.

3 According to the data of Spanish Ministry of Development.

4 Please also refer to the latest published sovereign analysis on Spain.

5 According to seasonally adjusted data of Spanish National Statistics Institute.

[Volver]

- “No tengo la habilidad de hace 30 o 40 años para disparar certero a un valor”

- Banco Sabadell rechaza la oferta de fusión de BBVA

- La asignación de los inversores extranjeros a las acciones estadounidenses es actualmente tan extrema como lo era en el pico mismo de la burbuja tecnológica

- “Por cada dólar invertido en combustibles fósiles, se están invirtiendo actualmente $1,7 en energías limpias”

- Las tasas de morosidad de las tarjetas de crédito en Estados Unidos se encuentran ahora en su nivel más alto registrado, según la Reserva Federal de Filadelfia

- La tasa de ahorro cae al 3,2% desde el 3,6% y desde el 5,2% de hace un año. Mientras tanto, los saldos de las tarjetas de crédito están en su punto más alto

- “No tengo la habilidad de hace 30 o 40 años para disparar certero a un valor”

- Las tasas de morosidad de las tarjetas de crédito en Estados Unidos se encuentran ahora en su nivel más alto registrado, según la Reserva Federal de Filadelfia

- La asignación de los inversores extranjeros a las acciones estadounidenses es actualmente tan extrema como lo era en el pico mismo de la burbuja tecnológica

- La tasa de ahorro cae al 3,2% desde el 3,6% y desde el 5,2% de hace un año. Mientras tanto, los saldos de las tarjetas de crédito están en su punto más alto

- Los fondos de acciones de China registraron su mayor entrada en 8 semanas, lo que indica una sensación predominante de optimismo entre los inversores con respecto a las acciones chinas

- Las asignaciones de efectivo de los gestores de fondos y los mínimos de varias décadas, lo que normalmente no es una buena señal para la rentabilidad de los activos en el futuro